How much do you really know about life insurance?

6 common misconceptionsMany of us are confused or misinformed about life insurance, including what it is, how it works, and how much it costs. So, to kickoff Life Insurance Awareness Month, we’re taking the opportunity to clear up six common misconceptions and help you plan for a more secure financial future.

Even though almost all employers offer their employees life insurance at no-cost as part of their benefits package, only a small percentage of employees consider buying more than that.

The truth is life insurance can be a strategic part of financial security. It provides money to your spouse or kids, for example, if you pass away unexpectedly or prematurely, so that they can continue to pay the bills that will likely fall on them when you’re gone. Not having enough money to pay those bills can not only cause undue hardship but also erode their financial wellness.

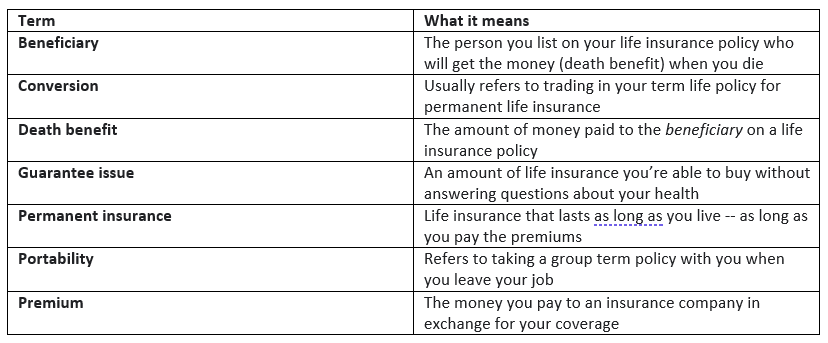

Last year, the Life Insurance Marketing Research Association (LIMRA) reported that barely one-third (31 percent) of Americans are very knowledgeable about life insurance. It certainly can seem complex, but let’s start with defining a few common terms associated with life insurance that can be a helpful reference for you.

MISCONCEPTION #1:

My employer already provides life insurance for free, so I don’t need any more.

REALITY:

Many employers typically offer a basic amount of life insurance to employees which is usually not going to be enough to cover major bills and expenses your loved ones would be left to pay on their own. According to LIMRA, the median basic coverage offered at the workplace is either a flat amount, like $20,000, or one times your salary. Would $20,000 be enough to cover what you owe on your home mortgage? Or the balance on your car loan(s)?

LIMRA states there are 102 million uninsured and underinsured Americans who need/need more life insurance coverage.

Industry experts suggest that individuals purchase about 10 times their income as a general rule of thumb. For example, if you earn $50,000 per year, that means you should consider having a total of $500,000 of life insurance protection.

MISCONCEPTION #2:

There is just one type of life insurance that covers me.

REALITY:

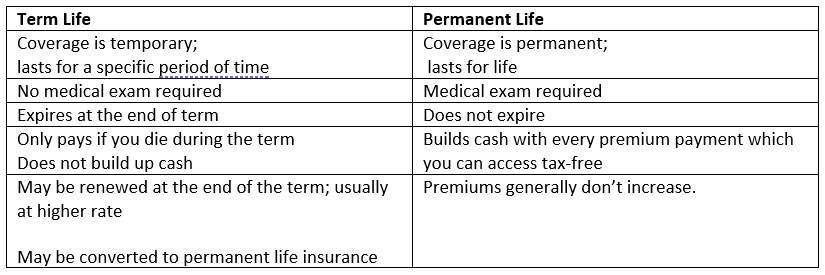

Generally speaking, there are two types of life insurance you can consider:

Term – which covers you for a definite term, say one year, and then expires

Permanent – which stays with you for life (unless you cancel it). It can build up cash with every premium payment you make, and over time, you can access or borrow against that sum to pay for other needs and goals while you’re alive.

Summary of key features for each type:

MISCONCEPTION #3:

I have too many bills to pay now. I can wait until I retire to buy life insurance and still be okay.

Reality:

Unfortunately, that is precisely the wrong time to buy it. Especially if you’ve been buying your life insurance through your employer. As stated earlier, the cost of life insurance goes up as you age. And once you retire from your employer, you may no longer be eligible to benefit from group rates and guaranteed issue policies.

One more thing to consider is that group term insurance you buy through an employer is not typically portable. So, the coverage won’t necessarily continue once you retire and leave your job. That is, unless you convert it to a permanent life insurance policy. But research shows that only a tiny percentage of workers ever convert their “term to perm”. That means they could be left without the life insurance coverage they thought they had at the time when it will be most expensive or cost-prohibitive for them to get.

One of the steps you can take to avoid becoming uninsured in your retirement years is to carefully review and consider your options to convert your term life to permanent life. Yes, your premium will increase, but the process should be quick and easy, and it doesn’t cost anything to do. By converting your policy to permanent coverage, you can retain life insurance for the rest of your life.

MISCONCEPTION #4:

I already have accidental death and dismemberment (AD&D) insurance, which will cover me.

Reality:

AD&D covers you with “living benefits” if you suffer a life-altering accident that results in the loss of one of your arms, legs, eyes, etc. It will also pay your beneficiaries if you die as a result of an unfortunate accident. But it will not pay anything if you happen to pass away from natural causes, sickness, drug overdose, etc.

Life insurance, on the other hand, will pay your beneficiaries upon your death. And that can bring you some welcome peace of mind since:

Almost half of households (48%) that only have workplace life insurance coverage say their families would struggle financially in less than six months should a wage earner die unexpectedly.

Source: LIMRA

MISCONCEPTION #5:

Life insurance is expensive. I can’t afford it.

Reality:

The truth is . . .you can’t afford not to have it. In fact, the younger you are, the more affordable it can be. But as you age, the cost increases at about eight-to-ten percent every year.

Millennials, in particular, overestimate the cost by 213 percent.

Of course, that’s true whether you purchase term life or permanent life insurance. But term insurance can be a solution during your working years. In many cases, it’s convenient to purchase through your workplace and it provides group rates and guaranteed issue, making it affordable and accessible. And it provides financial security for you and your family during critical years while you’re building savings and paying major household expenses.

MISCONCEPTION #6:

I’ve already saved money for my funeral.

Reality:

That’s a great first step. But what about other ongoing financial responsibilities that must still be paid once you’re gone, like credit card balances, student loans that are not forgiven, and college tuition payments for your kids?

Life insurance can help ensure they’ll have the funds necessary to pay the bills and give you the peace of mind that you’re taking care of them – even though you’re gone.

Our Life Insurance and Employee Benefits professionals are ready to help you navigate this critical part of your financial future. Contact us to learn more.

This material has been prepared for informational purposes only. BRP Group, Inc. and its affiliates, do not provide tax, legal or accounting advice. Please consult with your own tax, legal or accounting professionals before engaging in any transaction.

Download the Article

How much do you really know about life insurance?