Insuring College Students

Shopping for College? Mini Fridge… Check. Pillows… check. Proper Insurance Coverage… ?Does your student have all the essentials they need to start college in the fall?

Hint: Don’t just think socks and sheets.

Along with all the sweatshirts, books, snacks, bedding, computers, and other assorted gear you will be cramming into the car, make sure the proper insurance coverages travel with your child, as well. That’s right. We’re talking about insurance. Just because your son or daughter goes away doesn’t mean daily risks go away. “Anything can happen at any time” still applies.

For your reference, we’ve prioritized insurance coverages in this handy checklist that you may want to consider as you prepare for them to start a new chapter… away from home.

THE MUST-HAVES

Health insurance

Students will need health insurance. In fact, colleges and universities require it. The good news is you have several options for making sure they have coverage. They can:

- Remain on your family health insurance plan. They can be covered until they are 26 years old as long as your plan allows it. Since all plans have different rules and exemptions, double check with your insurance company or employer.

- Purchase a student health plan through their college or university

- Purchase coverage through the Health Insurance Marketplace established under the Patient Protection and Affordable Care Act.

Car insurance

If your student will be taking your car to college, even though it’s out of your driveway, it still needs to be insured. Usually, the least expensive option is to keep your student on the auto insurance policy you already have for your entire family. Just let your insurer know since the rate you pay and the amount of coverage you need may change, particularly if your student will now be the primary driver and possibly living in a different state than you do.

If your student does not take a car to college, it’s still a good idea to leave him or her on your policy so he or she can drive during extended breaks from school. It could even mean a discount on the policy since your student will be driving less.

What if your student’s care is titled in his or her own name and will be bringing it to college? In that case, the insurance must be in their name. While a separate policy can be expensive, your student can look into discounts for good-student, driver- training, and others which may lower the price tag.

THE SHOULD-HAVES

Renters Insurance

Today, no college student’s dorm room or apartment is complete without a laptop, printer, and other expensive items. So, make sure they are protected with the correct insurance.

If your student lives off campus and not in college-owned housing, your homeowner’s policy may not provide coverage (consult with your broker). But, for about $15 per month, a renter’s insurance policy can offer a broad layer of protection that can pay to replace personal items (see below) if they are ever damaged or stolen.

If your student lives in a dorm or school-owned housing, your own home insurance may automatically cover his or her personal items. Review your policy before they leave so you know what’s protected and if there are limits or deductibles. If you discover something is not covered by your existing policy, you may be able to add a rider for the extra protection you need.

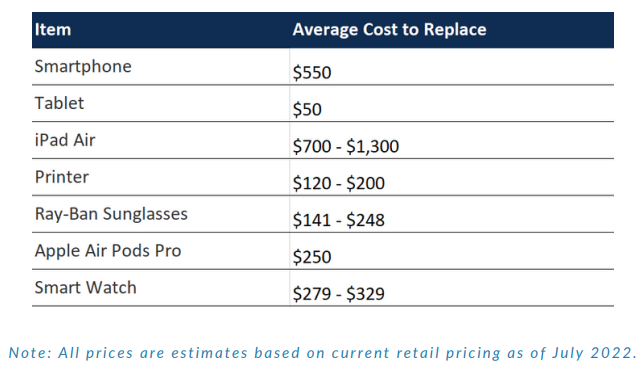

Here’s a sampling of how much it can cost to replace just a few of these items if they are stolen, damaged, or destroyed while your student is at college.

Tuition insurance

What if your college student must withdraw from school unexpectedly? Could you get tuition and fees that you paid upfront refunded? If you’re not sure, check what the school policy is for refunding tuition in the event your child must leave without receiving any academic credits for the semester.

If you find that the school’s tuition reimbursement policy is not as generous as you hoped, you may want to consider tuition insurance. For about $200 a semester, it can refund tuition, academic fees, room, board, and other expenses if your student withdraws before the end of the term due to a variety of reasons, including:

- Illness (ex. mononucleosis) or death.

- Injury (ex. car accident.)

- Debilitating mental health condition (ex. depression.)

- Loss of funding

Travel abroad insurance

For students who plan to study abroad, travel abroad insurance can offer advantages. Although every policy is different, this type of insurance covers common travel-related issues students may experience, including:

- Trip cancellation – can reimburse nonrefundable deposits for flights, hotels, etc., just in case there’s an illness or a death in the family, mandatory evacuation, a terrorist incident and/or bad weather that forces them to cancel.

- Missed flight connections – that results in missing a prepaid activity. Typically, coverage can either refund the cost of the missed one or pay the extra cost to take a different one.

- Trip interruption or delay – can pay for a hotel stay if, for instance, dangerous weather

grounds a flight. - Medical expenses, evacuation, and emergencies – to cover transportation costs back to the U.S. if your student gets sick or needs mandatory evacuation from a particular country.

- Lost or stolen baggage – can cover the value of the items that were lost or stolen. Some policies may also pay a daily stipend for things your student must buy while waiting for the bags to be returned to him or her.

- Passport recovery – can pay for fees to replace a lost or stolen passport.

THE NICE-TO-HAVES

Identity theft insurance

Unlocked dorm rooms, public Wi-Fi, heavy social media use, and carelessness are just some of the factors that put college students (and their personal information) at a greater risk for identity theft.

While there are simple things they can do to lessen the chances of falling victim to this crime, like using strong passwords, locking their doors, keeping personal documents out of sight (ex. Social Security number), in many cases these precautions will not completely stop a thief who is up to no good.

So, what can you do? For protection, you can consider identity theft insurance. Although policies differ, they can cover the cost of things like legal fees, phone calls, and credit monitoring, for example, which may be necessary to restore your student’s identity if it gets stolen.

Life insurance

Does your student have a student loan for which you co-signed?

Although we know you would rather not think about ever needing life insurance for your student, you can consider purchasing life insurance to cover the amount he or she may have borrowed. This way, if the unimaginable happens, the proceeds from the policy can repay the balance required by a lender.

There are several distinct types of life insurance, but term life could offer the most affordable protection since you could renew it every year you needed it, drop it if/when you’re removed as a co-signer, and hopefully, never need to use it.

Make sure your student has the protection they need while they’re away at college? Connect with us today to review your insurance options.

This material has been prepared for informational purposes only. BRP Group, Inc. and its affiliates, do not provide tax, legal or accounting advice. Please consult with your own tax, legal or accounting professionals before engaging in any transaction.

Download the Article

Shopping for College? Mini Fridge… Check. Pillows… check. Proper Insurance Coverage… ?