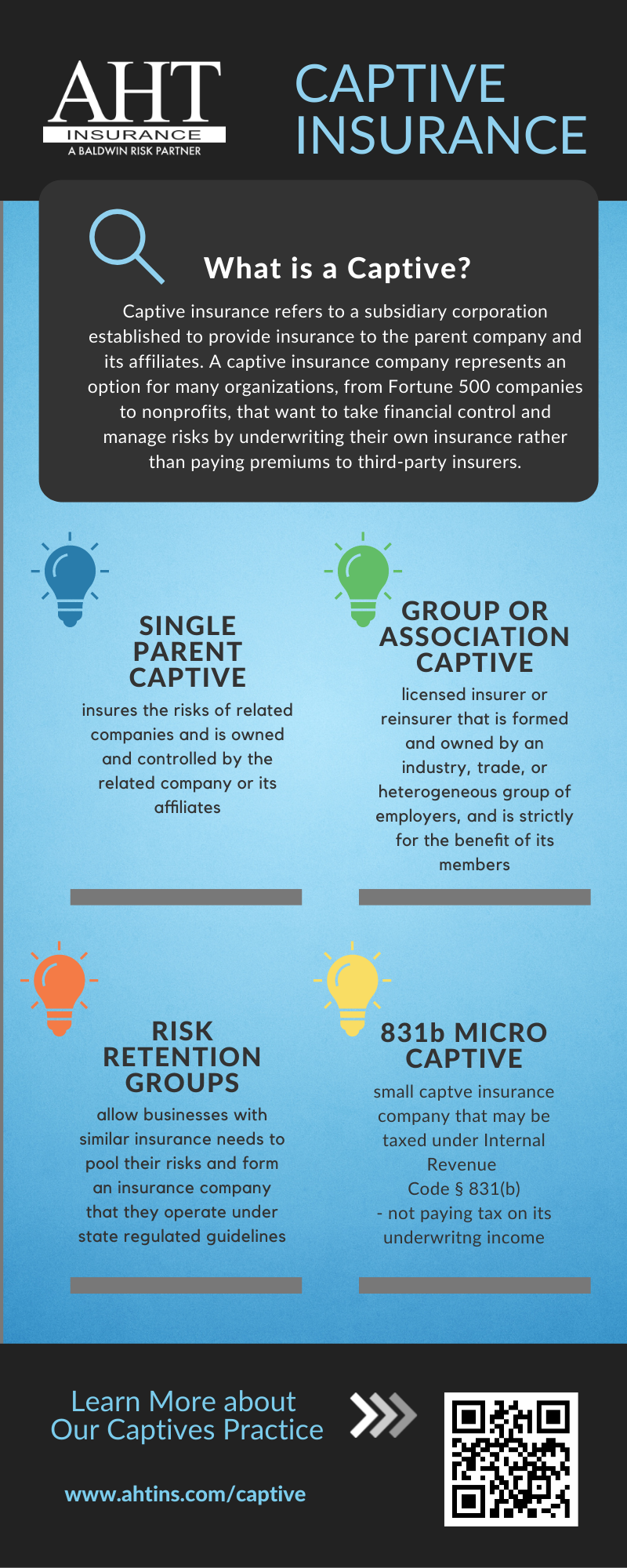

Captive FAQs

Q: What is a captive?

A: An insurance company that is wholly owned and controlled by its insureds, its primary purpose is to insure the risks of its owners and its insureds benefit from the captive’s underwriting profits.

Q: Who should consider a captive?

A: Financially stable companies with a good loss ratio, good claims history, and good risk management strategies, while willing to make a long-term commitment.

Q: What are the benefits of a captive’

A: Coverage tailored to meet your needs, reduce operating costs, capture underwriting profits, price stability, greater control of claims, flexibility in managing risk and program design, and accessibility to the reinsurance markets.

Q: What types of captives are there?

A: There are single-parent captives, group or association captives, segregated cell captives, agency captives and risk retention groups.

Q: Is there a minimum premium requirement?

A: There is no specific set minimum premium but there needs to be enough premium to cover administration costs and claims. $500,000 in annual premium would typically be a minimum premium.

Q: What coverages or product lines will a captive cover?

A: You can place most insurance lines in a captive, e.g., general liability, professional liability, excess and Umbrella coverage, property, supply chain, intellectual property, Trade Credit, environmental, Political risk, Product recall, terrorism, Errors and omissions, auto, worker’s compensation, employee benefits, etc.

Q: Are there any specific captive requirements?

A: You must have an independent actuarial study completed, ability to pay the required capital, captive must be formed as an insurance company designed to pay claims when necessary.

Q: How long do I need to stay in a Captive program, and can I leave the Captive’

A: There is no rule about how long a company is to stay in a captive, but captives are a long term alternative to the standard market. Yes, you may leave and dissolve the captive at anytime.

Q: How long do I need to stay in a Captive program, and can I leave the Captive?

A: There is no rule about how long a company is to stay in a captive, but captives are a long-term alternative to the standard market. Yes, you may leave and dissolve the captive at anytime.

Q: What investments can a Captive own to provide reserves?

A: A captive can own any investment approved by the insurance regulators in the jurisdiction where the captive insurance company is domiciled. It is important for the captive to maintain appropriate liquid reserves in order to meet potential claims liabilities. Therefore, captive insurance companies are highly regulated, and investment portfolios tend to be conservative and provide significant liquidity. Learn more at Oxford Risk Management Group.

Q: What is the time horizon for a Captive?

A: Any company considering forming a captive should have a long-term plan for the proper development and implementation of a captive program. Once the captive insurance company is established, an organization should consider modifications to their program as business and financial situations change. The insurance advisory team should meet at least annually to evaluate all aspects of the program to ensure ongoing success and benefits. If the insured maintains a favorable loss profile (the captive is successful in managing claims and expenses) it is possible for the captive’s investment portfolio to increase significantly over the years, because of the time value of money. Learn more at Oxford Risk Management Group.

Talk to us about additional frequently asked questions.

- Captives Overview – View Here

- What is a Captive? – View Here

- Is Captive Insurance Right for You? – View Here

{kind=link}

This material has been prepared for informational purposes only. BRP Group, Inc. and its affiliates, do not provide tax, legal or accounting advice. Please consult with your own tax, legal or accounting professionals before engaging in any transaction.

Download the Infographic

Captive FAQs