Creating a Caring Culture in the Looming Long-Term Care Crisis

By: Noel Evans - AHT Director of Long-Term Care Email NoelBy: Noel Evans, AHT Director of Long-Term Care

The looming long-term care crisis has arrived. We have working caregivers, their employers, and the impact long-term care has on family and finances. For employers and their employees, there is a way to create a caring culture in the workplace.

“To give somebody the permission to not have guilt about how they’re juggling work with the really trying job of caregiving — it’s indescribable. I don’t think anybody can know what it’s like until you go through it,” said Jackie Christie, a project manager for Richfield, MN based Best Buy as quoted in a Washington Post article, “The New Family Leave,” by Jena McGregor and Hannah Li.

Best Buy offers paid family caregiving leave of up to four weeks. As more employers and employees deal firsthand with the challenges of balancing a career and caregiving for loved ones, Long-Term Care Insurance is entering the mainstream. What do caregiving, paid family leave, group Long-Term Care Insurance, and other types of benefits that deal with these issues have in common?

The common ingredient is a loss of some type usually precipitates these. In some cases, it could be a family event like needing time off work because of the birth or adoption of a child. Significant family events require time off from work.

These events evoke a combination of emotions, love, grief, despair, stress, hopelessness, and denial.

Noel Evans

PH: 757.409.9065

Employee Benefits Have Positive Impact in the Workplace

All these work benefits provide an intangible and valuable benefit; peace-of-mind. For this article, I will focus on group Long-Term Care Insurance and caregiving resources. As Jackie Christie explains in the quote opening this article, caregiving benefits provide an indescribable relief.

In “The New Family Leave,” Carol Sladek, who runs Aon’s work-life consulting for human resources, remarks that employees, whether millennials or boomers, all are looking for benefits that extend beyond traditional family leave.

Creating a caring culture may vary from company to company, and each is dealing with different budgets and resources. However, in today’s workforce, with low unemployment and high demand for skilled workers, offering benefits like group Long-Term Care Insurance and paid family leave will help attract and retain these workers.

Group Long-Term Care Insurance Essential Due to Longevity

Group LTC Insurance (Group LTCi) is a bit different from paid family leave, bereavement leave, or disability, all of which offer an immediate benefit to the employee upon the triggering event.

If you have a newborn and your employer offers paid family leave, then you take off the desired and available time and recognize the value of that benefit immediately. If you are disabled and have employer offered Disability Insurance, you receive a check to replace that income for a short or long-term period once you meet the benefit trigger of the policy.

Recognizing the value of Group LTCi requires either a firsthand experience with a family member who needed long-term care, caregiving, or recognizing the consequences of having a family member that did not plan for extended care. Without this firsthand experience, helping the employees understand the value of Group LTCi requires a combination of education and employer support.

Advance Planning is Crucial

Advance planning offers valuable advantages; not only does it make the insurance less expensive, but it precludes being denied for diseases and health conditions that become more common as we age.

It is also a gift for you and your loved ones. By planning now, you are avoiding the mistakes that are accompanied by planning in a crisis. Planning for long-term care involves more than Long-Term Care Insurance; it includes legal and tax considerations. These considerations include issues like where you want to receive your future care and end-of-life and hospice concerns.

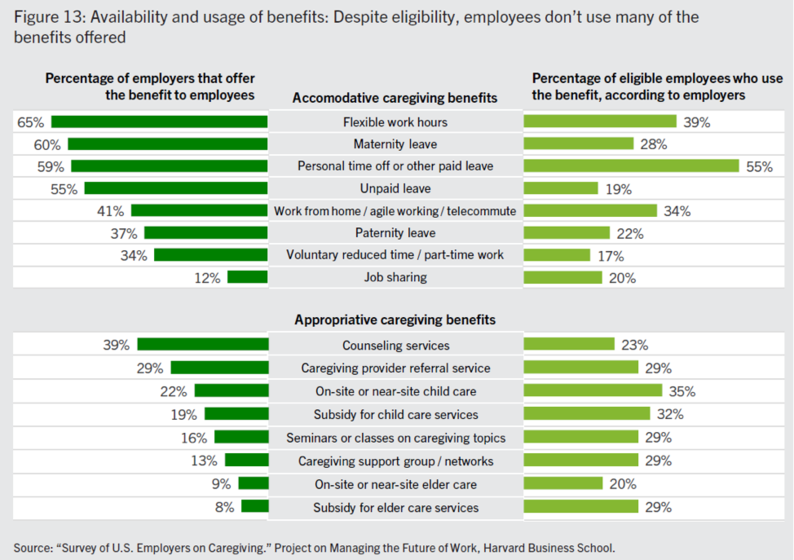

In their whitepaper, “The Caring Company; How employers can help employees manage their caregiving responsibilities-while reducing costs and increasing productivity,” Professor Joseph B. Fuller and Manjari Raman of Harvard Business School, warn of the caregiving crisis that is impacting employers, and employees, today.

Caregiving is Hard on Family Members

Fuller and Raman found that ¾ of U.S. workers are dealing with caregiving in some fashion, and most say that these responsibilities are hurting their productivity and earnings ability.

“The Caring Company” surveyed 1500 employees and 300 HR leaders and found that without employer support, many working caregivers were forced to reduce their work hours, limit career plans, or in some cases, leave the workforce altogether to care for a loved one. And those that left were comprised of highly skilled and compensated workers.

“By not offering benefits that employees actually want–and by not encouraging employees to use the benefits they do offer–companies incur millions of dollars of hidden costs due to employee turnover, loss of institutional knowledge, and temporary hiring,” Fuller and Raman note.

While the survey found that 29% of employers offer referrals to caregiving services, only 8% provided a subsidy for eldercare. Many employers will argue that they do offer generous benefits plans, but employees are looking for guidance like flexible work schedules, discounts for home care, counseling to relieve the burdens from caregiving, and Group LTCi.

Imagine an employee caring for a parent who did not adequately plan for long-term care and may not have the liquid assets to pay these exorbitant costs of care. Not only are they dealing with their own families and career demands, but now they must figure out how to pay these costs.

Many people decide to open their checkbooks and pay these costs. However, when family members do this it often impacts their ability to save for their future retirement and adversely impacts their ability to pay for their future care.

Group LTCi Benefits Multiple Generations

A correctly implemented Group LTCi plan can help not only the employee and their spouse/partner, but extended family as well, including parents, grandparents, siblings, and children. It should also include a robust Employee Assistance Program with caregiving services and a strong family leave/flexible work policy. The program should be properly marketed to the employees and their eligible family members.

Today’s Group LTCi is more affordable and flexible than ever, and whether the plan is funded fully or partially by the employer, or if it is a voluntary plan, it offers excellent value to the employer and the employee.

Employer-provided LTCi is treated as an accident and health plan, and as such, can be offered to a select group of employees and their spouses/partners, and eligible tax dependents, and are not included in the employee’s income.

Long-Term Care Insurance Offers Tax Benefits

The premiums paid through the company checkbook are deductible based on how the company is structured, whether a C-Corporation, including LLCs and Professional Corporations, taxed as a C-Corp., Sole Proprietors, Partner in a Partnership, 2% plus Shareholder of S-Corp., or LLC or Professional Corporation taxed as S-Corp. (read article on LTCi tax benefits by clicking here)

For example, a C- Corporation allows a 100% tax deduction of the premiums paid through the company checkbook for eligible employees. The tax treatment of LTCi Benefits is also very favorable in that tax-qualified LTC insurance reimbursement benefits for qualified long-term care expenses are not included as income.

Group LTC Insurance is very popular, especially among caregiving employees, and 82% of caregiving employees are interested in LTC insurance compared to 57% of the general population.

What are some other reasons that an employer would offer Long-Term Care Insurance in addition to the demand by caregivers and the tax benefits?

I spoke with Tom Rieske, Jr. of LTCi Partners, a company with decades of experience in the Group LTCi Market and he shared these tips:

- Timely and valuable education on the need for LTC planning. Getting old and planning for care is hard! People have a hard time envisioning being dependent in the future. Education can have an impact – just has employer education has helped with retirement planning.

- Addresses a significant “gap” in the employee’s financial plan and helps protect their 401(k). The biggest risk to a well thought out retirement plan is an unplanned health or long-term care need.

- Unisex rates and group discounts. An employer-based LTC plan provides gender-neutral multi-life rates that are generally lower than comparable coverage in the individual market. The rates in the individual market will be based on age, marital status, and state of residence.

- Ability to carve out select classes of employees. LTC Insurance can be offered in creative ways. For example, C-level executives could be offered a high benefit plan paid by the employer. Other executives and managers can buy meaningful standalone coverage, while younger employees can look at payroll deduct life insurance with LTC riders.

- Employees can pay for LTC Insurance through an HSA. HSAs are powerful tools that allow you to use funds in an HSA to pay LTCi premiums tax fee. A good strategy for some employees, if your plan is voluntary, is to look after retirement age and carve out some of your projected HSA funds to pay LTCi premiums.

My article was originally titled, “The Looming LTC Crisis has Arrived; Working Caregivers, their Employers, and how to Create a Caring Culture.” It sounds counter-intuitive, but the numbers support this.

For years as an advisor, I have read about the “looming” LTC crisis framed around our Boomer population, who will begin to turn 80 years old.

Risk of Needing Extended Care Increases with Age

In his article, “The 2020s Will Be A Tipping Point for Elder Care in the U.S.,” Howard Gleckman warns of how unprepared we are for caring for our aging Boomer population.

Gleckman writes that as people age, their risk of suffering from Alzheimer’s and dementia increases dramatically. He cites a National Institutes of Health estimate that says one-in-four of those 80 or older will have an Alzheimer’s or dementia diagnosis. Additionally, when it comes to Long-Term Care Insurance claims, 75% of claims are made by those 80 or above, and 45% by those 86 or above.

In 2025, just five years away, 75 plus million Baby Boomers will turn 80 years old, and this is when, typically, people begin to experience frailty, higher risks, and the need for support and services.

As the New Year rang in, I was reminded, it is 2020! We are at a tipping point in our need to care for our older adult population, but at the same time, I was reminded of personal experiences where friends and family needed care at much younger ages.

Try telling a working caregiver struggling to manage their career and family responsibilities that the crisis is looming. They are likely to say to you in no uncertain terms that it is, in fact, here.

Caregiving Will Become a Greater Burden on the American Family

Adding urgency and complexity to this crisis are studies that do not inspire confidence. The results of an aging population living much longer, reliance on unpaid caregivers, shortage of qualified, trained caregivers, and the changing family dynamic that has been impacted by declining marriage rates, increased divorce rates, and children who live far away from their parents, all point to challenges in receiving care.

In its study; “An Invisible Tsunami; “Aging Alone And its Effects on Older Americans, Families, and Taxpayers,” the United States Congress Joint Economic Committee found that, “In 1994, two-thirds (68 percent) of retiring adults lived within ten miles of an adult child. That share fell to 55 percent in 2014. In large part, this decline reflects falling fertility. The right axis of the figure indicates that the average number of children ever born to retiring adults fell from 3.1 in 1994 to 2.1 in 2014.”

This touches on the fact that many of my clients cite not being a burden as a critical driver of why they purchase LTCi, and with their children spread far geographically and dealing with their own careers and families, LTCi allows them to be companions rather than caregivers.

However, as daunting as these numbers are, there is a way to overcome these challenges by planning now. While I focus on Group LTCi in this article, the individual LTC Insurance market is another alternative for those who cannot access LTCi through their employer. It is strong and affordable, and flexible.

The impact of caregiving at the workplace will continue to grow with an aging population. Employers need to have a comprehensive strategy to address the effects on the employees both the problems they are having now and the future impact of the financial cost of care.

As Antione de Saint-Exupery said, “A goal without a plan is just a wish.” By planning properly, you can give your family a gift and gift yourself peace of mind, knowing that if you need care, you are protected, and your family won’t have to plan in crisis.